Why it works: Dominates searches like “backdoor Roth IRA 2025,” “backdoor Roth steps 2025,” “pro-rata rule backdoor Roth 2025,” “Roth IRA contribution deadline 2025.” Urgency from deadline + “ultimate guide” for clicks. Thought-provoking: “Locked out of direct Roth? This legal workaround could add thousands in tax-free growth.”

Detailed Structure & Content Outline:

1. Introduction

• Many high earners (e.g., MAGI over $150k single/$236k joint) can’t contribute directly to a Roth IRA for 2025 — but the backdoor Roth lets you bypass those limits entirely.

• Still 100% legal in 2025 (no changes from OBBBA or recent IRS rules).

• Key benefit: Contribute up to $7,000 ($8,000 if 50+ by Dec 31, 2025) for tax-free growth and withdrawals in retirement, no RMDs.

• Deadline: April 15, 2026 — act now during tax season!

2. 2025 Roth IRA Basics & Why Backdoor Matters

• Direct Roth limits: Phase-out starts at $150,000 MAGI single/Head of Household ($236,000 joint); full ineligibility at $165,000 single/$246,000 joint.

• Contribution limit (all IRAs combined): $7,000 under 50; $8,000 catch-up if 50+ by end of 2025.

• Traditional IRA contributions have no income limits — that’s the “back door.”

• Result: Non-deductible Traditional contribution → Roth conversion = tax-free Roth funds.

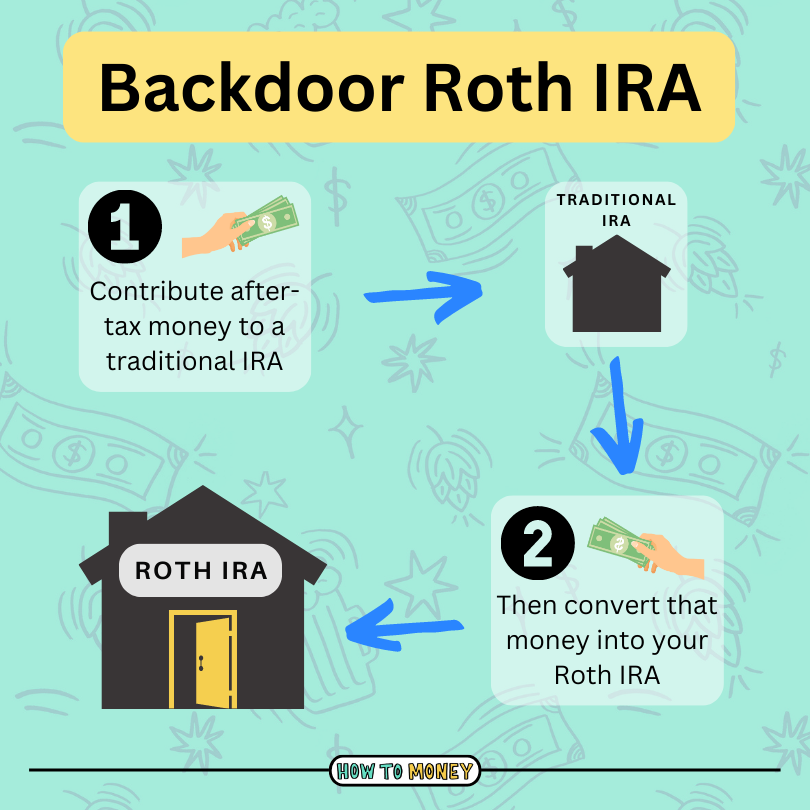

3. Step-by-Step Guide to Executing a Backdoor Roth for 2025

• Step 1: Confirm eligibility — Earned income ≥ contribution amount; no direct Roth if over limits.

• Step 2: Open (or use existing) Traditional IRA if needed. Contribute non-deductible amount (post-tax dollars) by April 15, 2026.

• Step 3: Convert to Roth IRA promptly (ideally same day/week to minimize earnings/tax). Use in-plan conversion or rollover.

• Step 4: Report on taxes — File Form 8606 (tracks non-deductible basis); include conversion on 2025 return (or 2026 if converted after filing).

• Step 5: Invest in Roth (stocks, ETFs, etc.) for long-term tax-free growth.

4. The Pro-Rata Rule: The Biggest Pitfall & How to Avoid It

• IRS treats all Traditional/SEPs/SIMPLE IRAs as one pool for conversions.

• Formula: Taxable portion = (Pre-tax balance / Total IRA balance) × Converted amount.

• Example 1 (Clean backdoor): $0 pre-tax IRAs + $7,000 non-deductible → Convert $7,000 = $0 taxable (ideal).

• Example 2 (Pro-rata trap): $100,000 pre-tax IRA + $7,000 non-deductible = $107,000 total. Convert $7,000 → ~93% taxable (~$6,510 tax hit).

• Workarounds: Roll pre-tax IRAs into 401(k)/employer plan first (if allowed); or avoid if you have old IRAs.

• Pro tip: Many do “clean” backdoors by keeping separate accounts or rolling out pre-tax funds.

5. Tax Implications & Reporting

• Non-deductible contribution: No upfront deduction.

• Conversion: Tax only on pre-tax/earnings portion (minimal if quick & clean).

• Earnings before conversion: Taxed as ordinary income.

• 5-year rule: For tax/penalty-free qualified withdrawals (applies per conversion).

• Required forms: Form 8606 (non-deductible + basis tracking); 1099-R/5498 from custodians.

6. Benefits vs. Risks

• Pros: Tax-free growth/withdrawals; no RMDs; estate planning perks; hedge against future tax hikes.

• Cons/Risks: Pro-rata surprises; potential future legislation (though intact now); small tax if earnings accrue; complexity (consult pro if IRAs exist).

• Best for: High earners (e.g., $200k+ single) with no/low pre-tax IRAs; long time horizon.

7. FAQs & Real-World Scenarios

• Can I do it every year? Yes — repeat annually.

• Spouse? Each can do separately.

• What if I already contributed direct Roth? Recharacterize or adjust.

Leave a Reply