Hey tax-savvy readers! With the 2025 tax year wrapping up and filing season underway in 2026, millions are navigating their returns amid major updates from the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025. This legislation made many 2017 Tax Cuts and Jobs Act (TCJA) provisions permanent, boosted some deductions, and introduced exciting new breaks—like deductions for tips, overtime, auto loan interest, and seniors—that apply directly to your 2025 income (filed now in 2026).

The core US federal income tax formula remains the same, but these changes can significantly lower your taxable income and boost refunds. Today, we’re breaking it down step by step, focusing exclusively on the 2025 tax year rules. Understanding “above-the-line” vs. “below-the-line” deductions is key—they’re your biggest levers for savings. Let’s dive in and explore how this could mean more money back in your pocket. Could one of these new deductions be your ticket to a bigger refund?

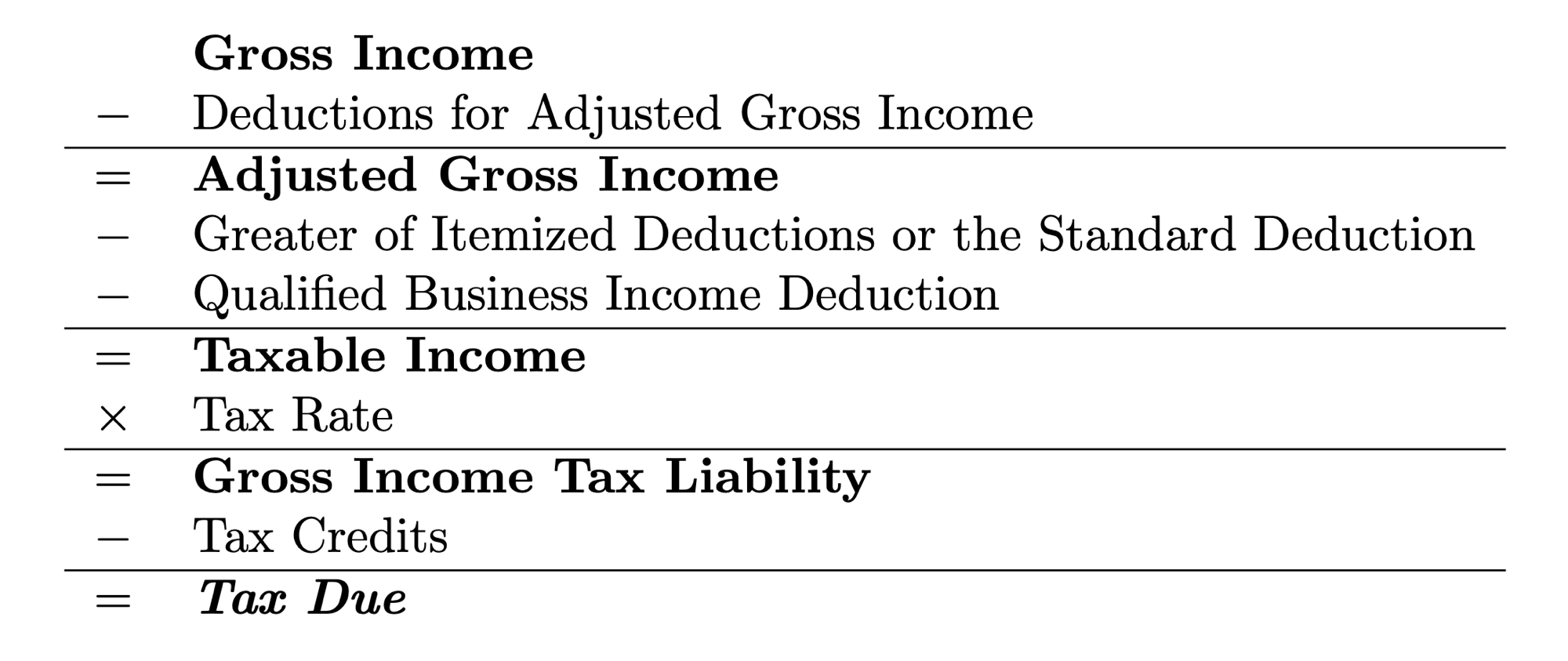

The Core Tax Formula for 2025

The IRS calculates your tax liability using this structured equation:

Total Gross Income (wages, tips, interest, business income, etc.)

− Above-the-Line Deductions (adjustments to income)

= Adjusted Gross Income (AGI)

AGI

− Below-the-Line Deductions (standard deduction or itemized deductions)

− Qualified Business Income Deduction (if eligible, up to 20% under Section 199A, made permanent)

= Taxable Income

Taxable Income × Applicable Tax Rates (progressive brackets)

= Tentative Tax

Tentative Tax

− Tax Credits (dollar-for-dollar reductions)

+ Other Taxes (e.g., self-employment tax)

= Final Tax Liability (subtract withholdings/estimated payments for refund or amount owed)

This progressive system taxes higher portions of income at higher rates. Lowering AGI or taxable income through deductions moves more of your income into lower brackets or qualifies you for credits.

Above-the-Line Deductions: Adjustments That Reduce AGI First (2025 Rules)

Above-the-line deductions (listed on Schedule 1 of Form 1040) subtract from gross income before AGI. This is powerful because AGI determines eligibility for many benefits (e.g., Roth IRA contributions, certain credits). You can claim these even if you take the standard deduction later—no itemizing required.

Common 2025 above-the-line deductions include:

• Student loan interest — Up to $2,500 (phased out at higher incomes).

• Educator expenses — Up to $300 for teachers’ classroom supplies.

• HSA contributions — Up to $4,150 (individual) or $8,300 (family) for high-deductible plans.

• Traditional IRA contributions — Up to $7,000 ($8,000 if 50+), subject to phase-outs.

• Self-employment tax adjustment — Deduct half of your self-employment taxes.

• Alimony (for pre-2019 agreements).

New OBBBA additions for 2025 (temporary through 2028, claimed on new Schedule 1-A):

• No Tax on Tips Deduction — Deduct up to $25,000 in qualified tips (voluntary cash/charged tips from customers in eligible occupations like servers, bartenders, gig workers). Reported on W-2, 1099, etc. Phases out for modified AGI over $150,000 (single) / $300,000 (joint). Self-employed limit: can’t exceed net business income.

• No Tax on Overtime Deduction — Deduct qualified overtime pay (premium portion, e.g., time-and-a-half excess) up to limits (details via IRS guidance; reported on W-2/1099).

• Auto Loan Interest Deduction — Deduct interest on loans for qualified personal vehicles (e.g., cars bought for personal use), with eligibility rules and caps.

• Senior Deduction — Extra $6,000 for those age 65+ (phases out at higher incomes, e.g., over $75,000 single / $150,000 joint in some estimates).

These new ones are game-changers for service workers, overtime earners, car owners, and seniors—directly reducing AGI regardless of standard/itemized choice.

Below-the-Line Deductions: From AGI to Taxable Income (2025 Rules)

After AGI, subtract below-the-line deductions (on Form 1040 lines after AGI). Choose the larger of:

• Standard Deduction (most popular, no receipts needed): For 2025 — $15,750 (single or married filing separately), $31,500 (married filing jointly), $23,625 (head of household). Add extra for age 65+ or blind (e.g., ~$1,600–$2,000 depending on status). OBBBA boosted these amounts and made the higher TCJA levels permanent.

• Itemized Deductions (Schedule A): If higher than standard, claim these:

• State and local taxes (SALT) — Cap temporarily raised to $40,000 (for incomes under certain thresholds; reverts later).

• Mortgage interest — On up to $750,000 debt.

• Medical expenses — Over 7.5% of AGI.

• Charitable contributions — Up to 60% of AGI for cash.

• Casualty/theft losses — Limited to disaster areas.

Note: Some new OBBBA deductions (tips, overtime, etc.) are above-the-line, so they stack with either standard or itemized.

Tax Brackets, Credits, and Final Calculation (2025)

Apply these 2025 federal income tax brackets (permanent under OBBBA) to taxable income:

For single filers (examples; full tables vary by status):

• 10%: $0 – $11,925

• 12%: $11,926 – $48,475

• 22%: $48,476 – $103,350

• 24%: $103,351 – $197,300

• And up to 37% for higher amounts.

Subtract credits (e.g., Child Tax Credit up to $2,200 per child, made permanent/enhanced; Earned Income Tax Credit). Add any other taxes.

Why Mastering This Matters for Your 2025 Return

OBBBA’s retroactive tweaks for 2025 (higher standard deduction, new deductions for tips/overtime/auto/seniors, permanent lower rates) could mean substantially lower taxes or bigger refunds—especially if you’re in service industries, work overtime, or are 65+. But IRS processing might be slower, so file early!

Quick tip: Gather 2025 docs (W-2s with tips/overtime noted, loan interest statements) and simulate your return using IRS tools or software. Overlooking an above-the-line move? It could drop your AGI and open more doors.

What 2025 deduction surprised you most? Drop it in the comments—we’ll tackle more mysteries next! Subscribe for daily tips, follow on X for #TTOTD, and let’s crush tax season together. 🚀

Leave a Reply